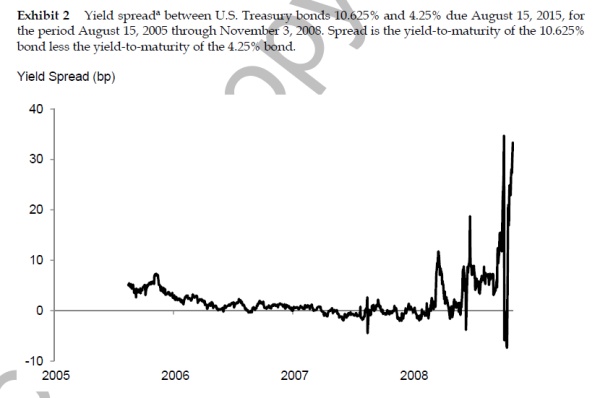

Sorry I was at the library so I cannot type Chinese here. I did some research on this question and would like to share my findings here. (Update: Sorry I just found out that neither of the two bonds are really on the run at that time, but since one is relatively new and liquid. So maybe this explanation still works.) This phenomenon is usually called "flight to liquidity". In normal time, both on/off the run treasury bonds can be used for financing in the Repo market rather interchangeably, although on the run bonds have a very little liquidity premium. While during crisis, people will strongly prefer on the run bonds due to the increasing macro uncertainty, which can be shown by the trading volume of these two bonds that day, as@Lenny Zhang has mentioned. Therefore magnify this liquidity premium significantly.

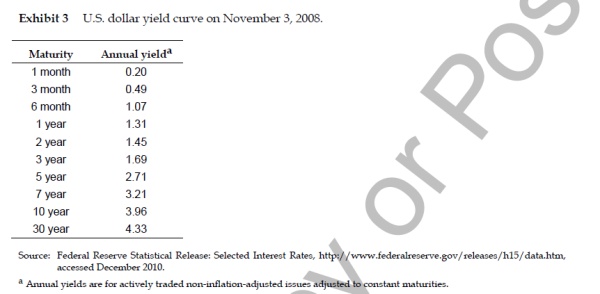

Actually similar phenomenon can also be observed during 1998 Ruble crisis, where the 30-yr T bond on the run premium rises from 4bps to 28bps. The main reason for "10��8�����������ֻ���ֻ��䵽��㸽��",I believe, is that the Fed lowered both discount rate and Fed Fund rate by 50bps the following day. BTW,there are many papers talking about the on/off the run premium. Just google it. But I still don't get the point of the last figure (The term structure one). Hope someone can shed some light on that. After your prof talked about this, please do share some thoughts with us. Many thanks!

Sources:http://personal.lse.ac.uk/vayanos/WPapers/FQFLPR.pdf Historical Changes of the Target Federal Funds and Discount Rates http://www.rmi.nus.edu.sg/_files/events/paper/Bond%20Liquidity%20Premia.pdf http://merage.uci.edu/~jorion/fixed/Sols-Ch5.pdf ===================================================== Updates: Since@Lenny Zhang mentioned that the indicators of trading liquidity of the two bonds are not available. I tried to get some clues from the Fed's website. After reading the Press Release on Oct 08,2008 which is the date they lowered the interest rates and the testimony of Bernanke on Oct 20,2008 to U.S. House of representatives. I think the money market turmoil is the cause of this spread. On Oct 20, Bernanke said "The financial turmoil intensified in recent weeks, as investors' confidence in banks and other financial institutions eroded and risk aversion heightened. Conditions in the interbank lending market have worsened, with term funding essentially unavailable. Withdrawals from prime money market mutual funds, which are important suppliers of credit to the commercial paper market, severely disrupted that market; and short-term credit, when available, has become much more costly for virtually all firms. "

Here is my interpretation. From his words we can infer that the money market credit was very tight at that time. Hence the demand for best collateral, namely on the run T-bonds, shot up. The Fed's following actions like TARP, lower rates and increase currency swap lines with foreign central banks ease this demand. That's why the spread went back a bit.

Updates 06/12/2013: @Lenny Zhang There is a field called "Estimated Traded Volume" and it is available for the two bonds. It surprised me that the volume for old bond is always higher than the relatively new one. I'm confused now. What do you think?

�����ҵ���ë���Ҹ��˸о�Ӧ����repo market�������ˣ�off the run low liquidity bond��repo market����Ǯ���ʱ����repo��on the run ���bps ����һ���������������roll down ����ȯ�ij��ڼ۸��Ҳ�������repo�������08���ʱ���г���ȫʧ�飬����repo marketֻԸ������liquid��bond��Ҳ�����⣬��Ϊ˭����֪�������Ǯ���˻�ᵹ�գ�������֮�����ŵ�û�������Ե�ȯ��ֻ�¾���90%discountҲ��һ����������������ty�������Ե����������off the run bondȥrepo�������Ҫ�100-200 bps���ܽ赽Ǯ����ô��������£�������ȯ��20-30bps��Ҳû��arbitrage����Ϊ��ĵ���ʵ����������õģ�repo market������function��������ȯ��Ǯ�ļ۸��converge��